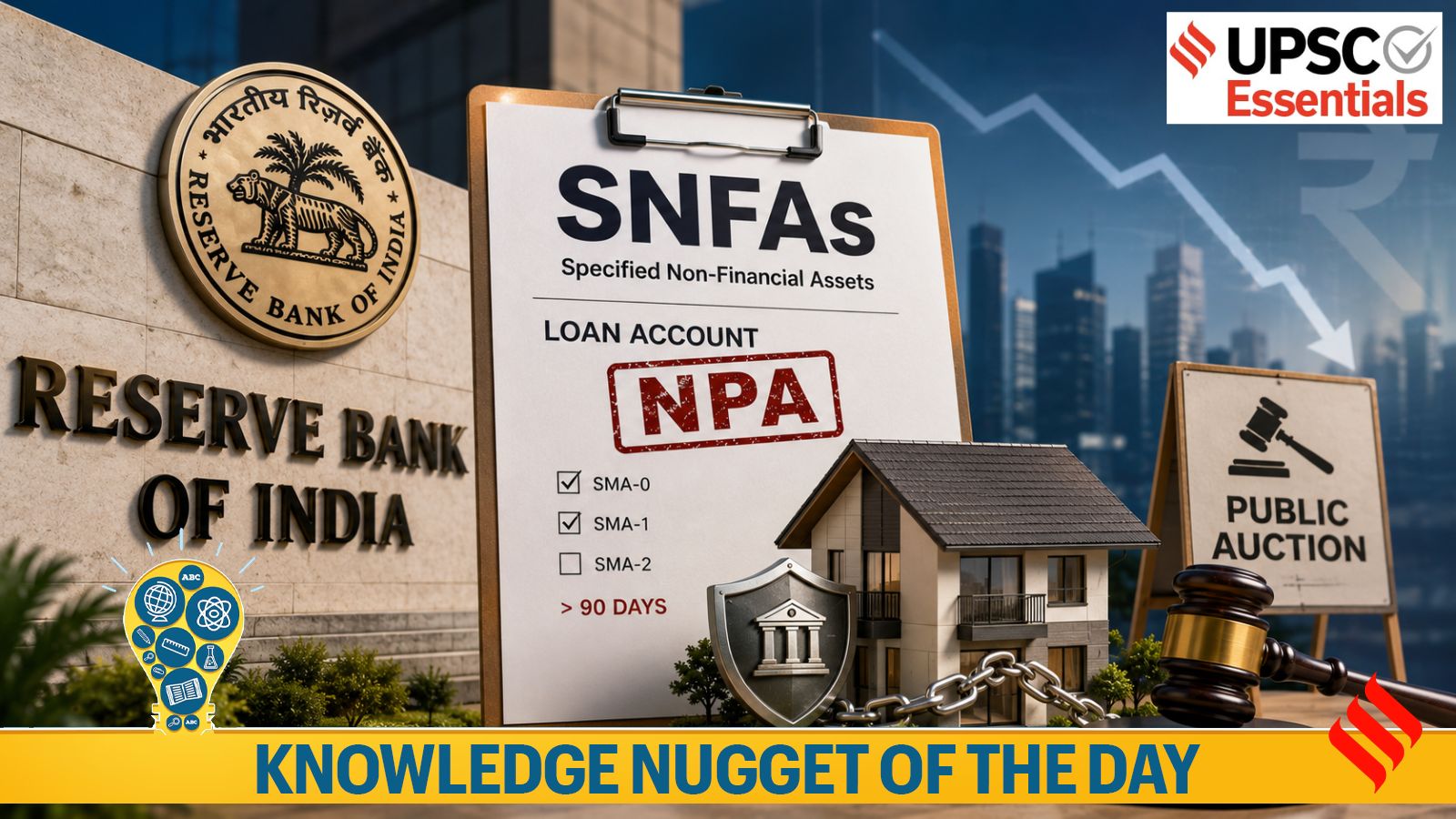

RBI Tightens Rules on Bank-Owned Properties: SNFAs and SARFAESI Act Explained

The Reserve Bank of India (RBI) has introduced new regulations concerning Specified Non-Financial Assets (SNFAs) that banks acquire from defaulting borrowers. These rules, part of the Third Amendment Directions, 2026, aim to standardise how banks handle such assets, ensuring transparency and preventing misuse.

SNFAs primarily include immovable properties like residential buildings, commercial properties, industrial land, and other real estate that banks accept as full or partial settlement of non-performing loans. Under the new framework, banks can acquire an SNFA only after a borrower's loan has been officially classified as a Non-Performing Asset (NPA). The acquisition must involve either full or partial settlement of the bank's outstanding exposure.

The RBI mandates that all commercial banks formulate a detailed internal policy governing the acquisition and disposal of SNFAs. This policy must specify eligibility criteria, approval procedures, and the recovery efforts to be attempted before acquiring a property. The disposal of such assets must primarily be through public auctions, following the principles of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002. Importantly, banks are prohibited from selling repossessed properties back to the original borrower or any related parties, even if the property later ceases to be classified as an SNFA.

Another key change is that SNFAs will no longer be counted as part of gross NPAs, net NPAs, or stressed assets. Instead, they will appear separately in bank balance sheets under the category 'non-banking assets acquired in satisfaction of claims.' This accounting change provides a clearer picture of a bank's asset quality.

Understanding NPAs and SARFAESI Act

A loan becomes a Non-Performing Asset (NPA) when the interest or principal remains unpaid for more than 90 days. Banks are required to identify incipient stress earlier through Special Mention Accounts (SMAs): SMA-0 (not due for more than 30 days but showing stress), SMA-1 (overdue 31-60 days), and SMA-2 (overdue 61-90 days). Once an account becomes NPA, it is classified as sub-standard (NPA for ≤12 months), doubtful (NPA >12 months), or loss (uncollectible).

The SARFAESI Act, enacted in 2002, allows banks and financial institutions to seize and sell the assets of defaulting borrowers without court intervention. It was introduced following recommendations by the Narasimham Committee and the Andhyarujina Committee to strengthen the banking sector against loan defaults. The new RBI directions align the disposal of SNFAs with SARFAESI principles, ensuring a transparent and efficient process.

These regulations aim to reduce the burden of non-performing assets on banks' balance sheets and promote faster resolution of stressed loans. By requiring public auctions and prohibiting sales back to defaulters, the RBI seeks to prevent asset stripping and ensure fair recovery.